![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/base/copper-d.gif)

|

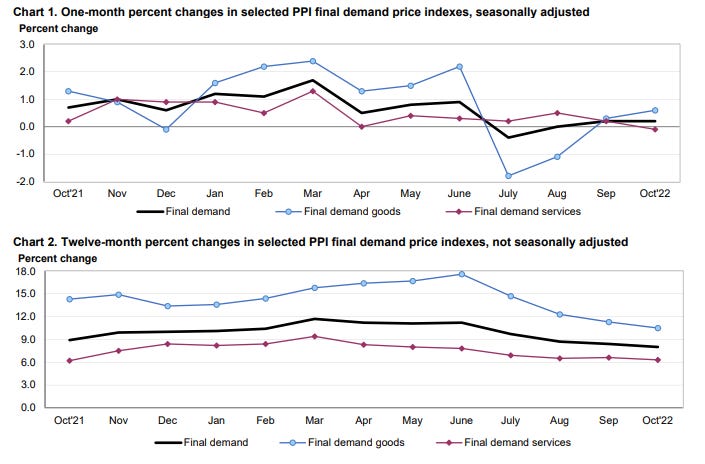

The October PPI report was bullish for stocks. The market should love than news and run higher this week, but there are signs of weakness. I was caught wrongfooted opening short positions yesterday, but I might have been early instead of wrong about the rally completing.

The exhaustion I saw in the market yesterday was wiped out by the morning’s response to the PPI. Most people are not looking at China and other data sets showing the clear tilt into deflation underway and more oncoming in 2023 once housing data trickles through. At least through the PPI release, the market is still viewing falling inflation as bullish.

The core PPI services segment went negative in October.

There’s one potential paradox: speculators have been bidding up commodity prices in response to lower inflation readings. Will that continue? Today’s initial response was a jump in commodity prices that quickly reversed. It will be telling how this plays out today. If copper and oil continue sliding, it may indicate the market has started realizing the downturn in prices and slowing pace of Federal Reserve rate hikes might not be bullish.

Stocks reacted far more positively because there’s no sign of recession yet. Falling commodities without a recession would be positive for GDP growth, consumer spending and limit Federal Reserve rate hikes. It would be a move back towards the “Goldilocks” economy that stocks love.

If instead stocks and commodities start sliding, it will be evidence the market has moved beyond inflation worries and started on deflation worries.

Yesterday I opened a bunch of short positions having seen exhaustion on the tape. I’m going to be underwater at the open, but notice the line on the NQ chart. I have two resistance lines on the NQ at 12100 and 12200. Right here, my thinking is to add more shorts at 12200 if it can get there, but cut loose all the short positions above.

Commodities exploded higher on Friday. Market participants and more so financial media, always create an explanation for what happened. The story for Friday's move was China re-opening.

Another explanation is that the money printers take power away from the Federal Reserve. There is a growing rumor that the Treasury Department led by former Fed chair Janet Yellen will seize monetary power. She has floated the idea of doing a "twist" where the treasury issues new debt and buys back older debts. This would squeeze shorts and shock the market in the short-term, though maybe not. First, if this is done, it is the financial equivalent of draining the SPR for votes. How many votes will the Biden administration get for the SPR policy? It looks like a negative number to me. I bet this move is a larger negative number. It wants to "drain" the treasury market of very favorable debt (from the view of the U.S. government) and replace it with more volatile short-term debt that will reset at higher interest rates. As with the SPR drain, they refuse the simple solution: issue less debt. Instead of sending $30 billion to Ukraine, issue $30 billion less in treasuries. What a concept! As with the SPR drain, if the policy fails and the future is worse, then they've screwed the country. Interest on the debt will bring forward the date when massive cuts in welfare and warfare spending will be made.

It's possible the gambit will fail immediately too. In addition to worsening the government's fiscal position, they are crossing a red line by interfering in monetary policy. As someone who opposes central banks for economic and political reasons, it nonetheless is a superior economic arrangement to a U.S. treasury run by literal money printing MMTers. It is possible the market reaction to this treasury move will be a collapse in treasuries, the U.S. dollar and an outbreak of inflation so bad that there are inflation riots in the streets. For this potential risk alone, it is insane for a Democrat administration to effectively take 100 percent responsibility for the nation's fiscal woes built up over generations, but that is what will be the "narrative" if they do it.

The above scenario is a valid explanation for a sustained explosion in commodities of which Friday was merely the start. Another is that for all the whining by degenerate speculators and gamblers, the Federal Reserve still has interest rates at negative 2 percent measured by core CPI. What if I and others who expect lower inflation are wrong? If neutral policy includes rates of positive 2 percent, that argues for an 8 percent Fed funds rate right now. That would mean mortgages above 10 percent. What if the move on Friday was the market calling bullshit on the Fed and inflation is about to rip higher? Say hello to 10 percent on the 10-year and 15 percent yield on mortgages.

Intuitively it makes sense. There is no hope of a soft landing given the amount of debt-financed stimulus and lockdowns that preceded it. At the very least, the 30 to 50 percent rise in home prices, more than 100 percent in many places, should reverse nearly 100 percent if the inflation comes out. Factor in lockdowns and the economy should be at a lower level than it was in February 2020. There was a great deal of economic destruction carried out by politicians and then hidden by massive stimulus. The electoral guillotine that will drop on Tuesday November 8 is the public reaction to the tip of an iceberg of destruction that the ruling class sent our way in 2020.

Alright, there's your commodities bull case. How about the bear case? First, the Fed gets serious about inflation if the runaway inflation scenario is real. They do whatever it takes to get inflation down, including the hardest landing for stocks since 1929. You will hear screeching like never before if the Fed does an emergency rate hike, but it is the appropriate move if commodities are taking off. Copper is begging for a 100 basis point emerging hike if it has one more day like Friday.

More likely, the big move is the end of a speculative wave. Whenever I'm writing one of these posts, something big usually follows. Markets get to the starting line of a major phase change many times before they go through with the change. If this isn't the phase change yet, then history says Friday was a great shorting opportunity.

Prior spikes in copper, outside of the Ukraine war pop, came at the end of rallies:

.jpg)

.jpg)

.jpg)

.jpg)

Chinese local governments should make better use of state-owned assets, such as houses, land and cars, in order to help plug the gap between fiscal revenue and expenditure, the Ministry of Finance said.Liu He had a widely-discussed editorial calling for supply side reforms: 刘鹤人民日报撰文:把实施扩大内需战略同深化供给侧结构性改革有机结合起来Hong Kong shares jumped 5 percent and A-shares more than 2 percent with more rumors of reopening. These two hotpot chains sport higher lows.Local governments should conduct a thorough inventory of the assets that they occupy and use to make sure that they are being used efficiently, such as through the sharing, swapping, leasing or selling of these resources, and that none are lying idle, the ministry said in a document released yesterday.

The above is a premium post at ZeroHedge, but comes on the heels of a relentless string of very bullish calls from all over finance. Not only are bulls bullish, but bears also are talking about a melt-up. This JPM headline makes me wonder if Wall Street isn't trying to dump as much as possible though.

Anything can happen in markets. Anything. Maybe bears are focusing on gold and copper instead of stocks because of the strength in stocks. Maybe bulls are focused on stocks and that's causing a divergence. Maybe bulls are right and the Fed will pivot or Powell will touch his face in a way that means stocks go up 10 percent. Sentiment is funny, that's why you have to pay attention to how stocks react on news items. The market is clearly in a very bullish and optimistic mood at the moment. I look out over the coming months and even years, and do not see how the Fed pivots or pauses. If anything, I expect the opposite. If they ease too early, they'll blow it the same way the 1970s Fed did. The risk of stagflation would climb. Bonds would eventually reject the pivot and sell off, forcing the Fed to chase the market interest rates.

In the 1970s the Fed cut rates midway through the recessions and that was the wrong move. Not repeating would mean the Fed hikes rates until a recession is evident (the recesion will likely be backdated) and then refuses any rate cuts or moves very slowly such that rates are still high at the end of the recession.

To sum it up, I don't hope for a fall. I don't see how it can rise for very long and if it rises, then it's more profit for the bears on the eventual downswing.

Stepping back a bit, about the only market "signaling" a pivot is the most solipsitic one: stocks.

ZB is heading for the measured move target of 121. TLT is in free fall. I do not know if 121 will hold or not. I'm agnostic here. As I've said before, I think ZB can bounce as stocks crater and it can bounce with a bull rally. If it is falling, then stock are probably going lower. ZB is at a new 52-week low. Don't over think it.